Four different ways to spend an inheritance, and how a Kellands financial planner can help

If you receive an inheritance, you might be wondering how to use these funds. Read four ways to spend your inheritance with the help of a financial planner.

The grief of losing a parent or other close relative can be difficult to bear – and on top of it all, you may need to deal with the ins and outs of this person’s finances during a hard time.

If you have recently come into significant wealth through an inheritance, you could feel overwhelmed by the level of responsibility this money brings. If so, you’re not the only one.

Indeed, the Institute for Fiscal Studies reported in 2020 that wealth-to-income ratios are increasing – and this is largely due to the wealth being passed down from generation to generation.

For example, the study shows the inheritance received by those born in the 1960s will represent 8% of their lifetime earnings. Amazingly, this figure increases to 14% for those born in the 1980s.

So, as the amount of wealth being passed down slowly increases, knowing how you could manage a large influx of capital is vitally important.

Read on to find out four ways you could spend your inheritance, and how each one could help further your goals.

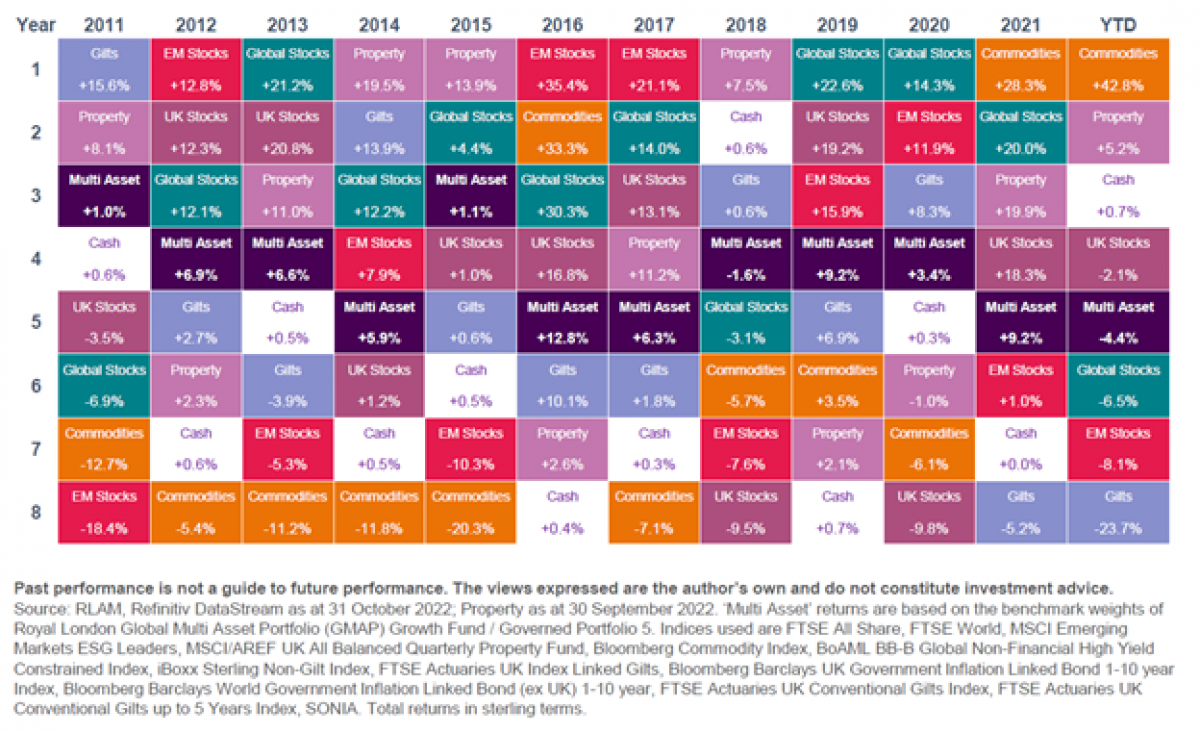

1. Invest your inherited wealth in the stock market

If you are comfortably living from your own income and do not need to support your day-to-day life with the inheritance you’ve received, you could be thinking: “how can I put this wealth away for later in life?”

There is, of course, more than one way to save your inheritance for the future, and one effective way could be to invest some or all of the wealth.

Indeed, while investing does pose some risk to your wealth in most cases, it can also offer the potential to protect your money from the effects of inflation.

For instance, according to The Times Money Mentor, if you had £100,000 left in cash earning no interest seeing an average inflation rate of 2% a year, the sum would only be “worth” £66,761 after 20 years.

Whereas, investing part of your inheritance in a diverse portfolio of assets that meets your appetite for risk could improve its long-term spending power.

2. Expand your property portfolio

Another way to invest your inheritance would be to expand your property portfolio. Perhaps you’ve always wanted a bolthole by the sea, or wish to support your income with a buy-to-let business.

Whatever your reason for investing further in property, this move could keep your inherited wealth locked into a valuable asset for the years to come.

While there is risk associated with any investment – the property market could crash, or the home could cost you more in maintenance and bills than you had anticipated – overall, your property is likely to appreciate in value over time.

The below table from the Office for National Statistics (ONS) exemplifies the gradual overall rise in UK house prices between January 2005 and December 2022.

Source: ONS

So, while past performance is not a reliable indicator of future performance, investing your inheritance in property could provide you with a valuable asset to rely on in future years.

3. Pass your inheritance straight to the next generation

If you have inherited money that you feel your children would benefit from, there are ways to bypass your own inheritance and pass it straight to the next generation.

Your adult children may be looking to start their own families, get married, buy their first home, or climb the career ladder from the bottom rung up – all of which could be helped by this injection of capital.

Some options for passing on your inherited wealth include:

· Writing the funds into trust. This can usually protect the wealth you pass down from Inheritance Tax (IHT), and can give the trustee full control over how the money is used.

· Investing the money on your child’s behalf. For instance, if your child is looking to buy their first home, providing a sizeable deposit from the inheritance you receive can help them build a nest egg of their own.

· Writing a Deed of Variation into your will. This is a legal document that allows beneficiaries named in a will to make changes to the distribution of an estate. So, if you already have wealth of your own, and are due to receive an inheritance that could perhaps lead to IHT issues, a Deed of Variation allows you to redirect part or all of an inheritance to another person (such as an adult child). This can help to reduce the amount of IHT payable on this portion of an estate.

· Giving the funds. You can pass up to £3,000 a year tax-efficiently to anyone you like. If you give more than £3,000 to your loved ones in a single tax year, they may pay IHT on the sum if you pass away within seven years.

If you do choose this route, it could be wise to consult your Kellands financial planner before immediately passing on the funds. Without professional advice, you or your children could pay an increased tax bill as a result, depleting your inherited wealth unnecessarily.

4. Pay the funds into your pension

Finally, if you are still approaching retirement, you could wish to boost your later-life income by paying your inheritance into your pension.

If you are still a little way away from retiring, contributing a larger sum each year between now and when you draw your funds could improve your financial stability in retirement – especially as you’ll likely benefit from tax relief on your contributions.

If you plan to reroute your inheritance into your pension, speak to your Kellands financial planner before you proceed.

We can review your current circumstances, advise on the tax implications of your decision, and help form a tax-efficient contribution plan.

Get in touch

For advice on incorporating your inheritance into a bespoke financial plan, speak to us today. Email us at hale@kelland.co.uk, or call 0161 929 8838.

Please note

This article is for information only. Please do not act based on anything you might read in this article. All contents are based on our understanding of HMRC legislation, which is subject to change.

The value of your investment can go down as well as up and you may not get back the full amount you invested. Past performance is not a reliable indicator of future performance.

Your home may be repossessed if you do not keep up repayments on a mortgage or other loans secured on it. Buy-to-let (pure) and commercial mortgages are not regulated by the FCA. Think carefully before securing other debts against your home.

The Financial Conduct Authority does not regulate estate planning, tax planning or will writing.

A pension is a long-term investment not normally accessible until 55 (57 from April 2028). The fund value may fluctuate and can go down, which would have an impact on the level of pension benefits available. Past performance is not a reliable indicator of future results.

The tax implications of pension withdrawals will be based on your individual circumstances. Thresholds, percentage rates and tax legislation may change in subsequent Finance Acts.